The DTC VSC Market in 2026: Why the Fastest-Growing F&I Channel Is Just Getting Started

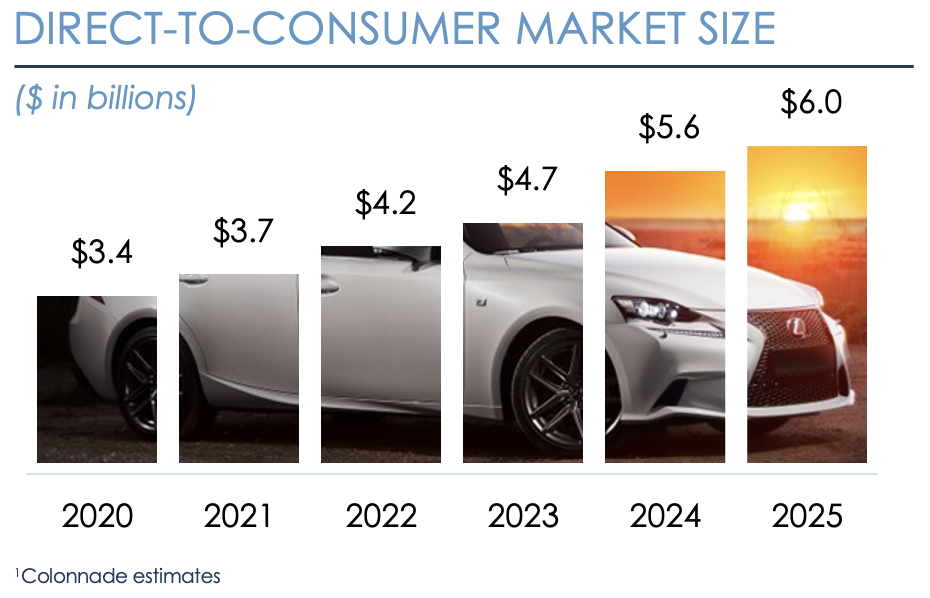

The DTC VSC industry is no longer an emerging channel. It has reached a level of scale and maturity that is attracting institutional attention. Colonnade Advisors, an independent investment bank focused on financial and business services, published a March 2026 whitepaper confirming what marketers are already seeing in their numbers: DTC VSC is the fastest-growing segment of automotive F&I, expanding at a 12.3% CAGR.

For marketers, this is confirmation that the growth is structural, not cyclical. The forces driving the channel are embedded in the economics of vehicle ownership, the aging vehicle fleet, and the behavior of consumers who need coverage but did not purchase it at the point of sale.

Contents

What Drives a 12.3% CAGR

The DTC VSC channel is not growing because of a favorable marketing environment. It is growing because it solves a financial problem that is getting worse.

More than 90% of U.S. households own a vehicle. When it breaks, it gets repaired. That creates inelastic demand for repair and, by extension, for products that smooth that cost.

A VSC converts a variable, often unpredictable expense into a fixed monthly payment. In a market where 58% of vehicle owners cannot absorb a $1,000 repair, that is not a discretionary product. It is budget protection.

The addressable market remains large. There are approximately 296.5 million passenger vehicles on U.S. roads, roughly 70% of which fall within the core coverage window. Of those eligible vehicles, only 44% carry any VSC coverage.

That means the majority of the market is not a competitive displacement problem. It is a coverage gap.

The Opportunity in Under-penetrated Coverage

The product sold in the DTC channel and the product sold at the dealership are substantively the same. The difference is timing.

Consumers who did not purchase coverage at the point of sale, or whose coverage has lapsed, represent the DTC market.

DTC marketers reach this population through direct mail, email, digital advertising, television, and radio. Direct mail remains particularly effective because VSCs are complex, infrequently purchased, and relatively high-priced products that benefit from detailed, targeted communication.

A typical VSC is priced between $3,500 and $4,000 for five years of coverage. When sold through the DTC channel, installment structures expand the addressable market by reducing upfront cost friction and improving conversion among consumers who need coverage but cannot absorb a lump-sum payment.

Five Structural Trends Shaping Demand

Colonnade identifies five trends driving sustained demand in the DTC VSC market. These trends do not operate independently. They compound into one outcome: higher repair exposure on an aging fleet with less financial flexibility to absorb it.

Vehicle ownership is getting more expensive faster than income. Since 2020, wages have grown 30% and vehicle prices 20%, but maintenance and repair costs have increased 46%. Car repair has become a major financial concern for many consumers, with many common repairs exceeding $1,000.

Repair costs are rising faster than inflation. Modern vehicles are more complex to diagnose and repair. Advanced electronics, driver assistance systems, and evolving powertrains increase both labor time and parts costs. Since August 2022, repair costs have risen 13.9% and maintenance costs 10.9%, compared to 5.6% for general inflation. Technician wages have increased more than 41% since 2001 due to persistent labor shortages.

The vehicle fleet is aging. The average vehicle age in the U.S. is now 12.8 years. As new vehicles become less affordable, consumers are holding onto cars longer. Older vehicles require more frequent and more expensive repairs.

Financing is extending the ownership cycle. The average used vehicle loan term increased from 64 months in 2018 to 69 months in 2025. Payments have grown faster than wages, and vehicle-related expenses now account for approximately 18% of monthly income. For many consumers, replacing a vehicle is not economically viable, increasing reliance on maintaining existing vehicles.

Dealer remarketing is unlocking incremental opportunity. Only 45% of new car buyers purchase a VSC at the point of sale. Dealer remarketing programs allow DTC marketers to access known customers with known vehicles, improving targeting and lowering acquisition costs while expanding the reachable market.

The DTC Channel’s Competitive Advantage

The DTC VSC model is attractive across key financial dimensions. Margins are high, cash flow is recurring through installment payments, and the model scales efficiently with marketing investment. The market remains fragmented, which makes share gain achievable without requiring overall market expansion.

There is, however, a structural difference in how DTC contracts behave. Because payments are visible as standalone line items, consumers are more aware of the cost. That visibility drives higher cancellation rates in the DTC channel relative to dealership sales.

The difference is not just the cancellation rate. It is the timing.

Two channels can show the same cancellation rate and produce very different economics depending on when those cancellations occur. Understanding how cancellations develop across the life of a cohort is a core operating requirement in the DTC channel.

Why M&A Attention Is Following the Growth

Historically, M&A activity in automotive F&I concentrated in the dealership channel, where scale and infrastructure were already established.

That is changing. As DTC firms build scale, compliance frameworks, and operational infrastructure, the segment has reached a level where it attracts institutional attention from both strategic acquirers and financial sponsors.

Colonnade’s framing of the DTC VSC market reflects that shift. For firms, this is both validation and a signal. The data and operating discipline required to compete in this market are the same data and structures buyers expect to see in diligence.

What This Means for DTC VSC Marketers

The structural case is clear. The market is growing at a 12.3% CAGR, more than half of eligible vehicles remain uncovered, and the underlying demand drivers are not cyclical.

The implication for marketers is simple.

This is a market where structural growth exists, but execution still determines who captures it.

The marketers best positioned to capture that growth are the ones with strong acquisition economics, retention discipline, and operating visibility. They understand where acquisition is working, how cancellations develop, and how the lifetime economics of each segment perform.

Growth in this market rewards marketers who understand their cohorts, not just their totals.

Sources

- Colonnade Advisors, Direct-to-Consumer VSC Industry, March 2026

- ANA Response Rate Report

- Experian

- NADA, Cox Automotive, StoneEagle

- United States Census Bureau

- FinanceBuzz

- Federal Reserve Bank of St. Louis (FRED)

- U.S. Bureau of Labor Statistics

- The Zebra

- Kelley Blue Book

- MarketWatch

- Minneapolis Fed