DealerTech AI in Warranty Claims: From Processing to Decision Systems

OEM warranty claims processing is one of the largest manual revenue functions in automotive retail. DealerTech AI in warranty claims is changing how revenue is processed, validated, and recovered across dealership operations. Most OEMs runs their own proprietary claims system. An incorrect submission, a wrong labor code, a missing authorization, a documentation gap, results in rejection or delayed revenue. The people navigating this process are doing it claim by claim, system by system, largely by hand.

That is the baseline. And it is changing faster than most of the industry realizes.

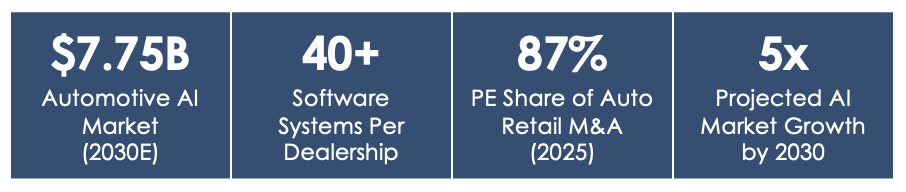

The automotive AI market in dealerships is projected to grow from $1.4 billion in 2023 to $7.75 billion by 2030 — a roughly 5x expansion fueled by AI adoption across four distinct capability categories. Private equity captured 87% of auto retail M&A activity in 2025, and the deals are concentrated in the same categories where documented ROI already exists. Warranty and claims AI is one of them. It is also, by a significant margin, the least covered in trade press relative to the returns it is generating.

The Dealership Data Problem AI Is Solving

A franchised dealership generates continuous transaction data across vehicle sales, financing, service, parts, and warranty. It also can run on more than 40 separate software systems that typically do not communicate with one another. The data exists. The problem is that it has never been unified, structured, or activated across departments in any coherent way.

That fragmentation is precisely what makes the current AI investment cycle structurally different from prior rounds of dealertech investment. Earlier platforms added systems to the stack. The companies attracting capital today are building the connective tissue between them, unifying dealer data into a shared intelligence layer that enables faster decisions, better pricing, and automated workflows that were previously impossible.

For warranty operations specifically, the implication is direct: AI doesn’t just speed up the existing process. It changes what the process is.

Warranty and Claims AI: The Highest ROI Category Nobody Is Talking About

The framing from the Warranty Innovations 2025 conference was precise: TPAs are evolving from transaction processors to decision intelligence hubs. Human roles are shifting from repetitive processing to exception management.

That transition is already producing measurable results. In documented deployments, AI warranty claims processing has delivered:

- A 32% reduction in manually processed claims

- A 16% improvement in processing time

- An increase in the share of claims identified with deficiencies from 25% to 42%

(Source: MSX International)

The last number is the one worth sitting with. AI isn’t just processing the same claims faster, it is catching errors and anomalies that the prior manual process was consistently missing. That is a different kind of value. It is not efficiency. It is accuracy at a scale that human review cannot replicate.

AI fraud detection makes this explicit: systems can now identify patterns across multiple vehicle models and repair facilities simultaneously. A single faulty part generating warranty claims across an entire model year becomes visible in an AI-analyzed dataset in a way that is simply invisible when a human reviewer is working claim by claim. The leakage that manual processing accepts as structural, AI treats as a solvable problem.

Where the Rest of the AI Stack Intersects F&I

Warranty claims are not the only place where the transformation reaches F&I professionals. Three other capability categories in the dealertech AI landscape have direct implications for how the F&I desk operates.

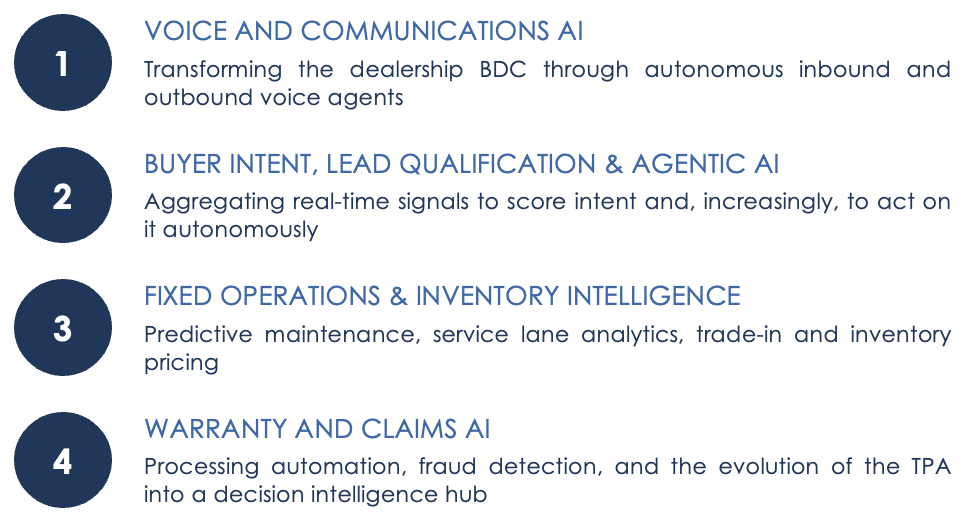

Voice and communications AI is the most commercially mature category. Dealerships currently miss an estimated 30–40% of inbound calls. AI voice agents replace legacy BDC infrastructure at a fraction of the cost, with sub-2-second response latency that customers cannot distinguish from a live representative — a documented technical threshold, not a marketing claim. The dealers deploying outbound AI for lease maturities, open recalls, and equity mining are generating appointment volumes that are structurally different from what floor-walk traffic alone can produce.

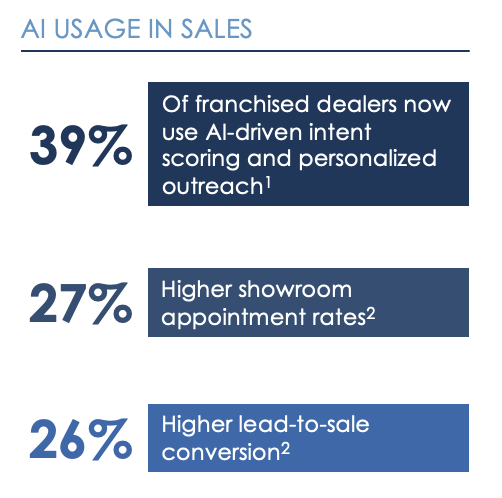

Buyer intent and agentic AI is the category attracting the most growth equity. Among franchised dealers now using AI-driven intent scoring, results show 27% higher showroom appointment rates and 26% higher lead-to-sale conversion compared to non-AI workflows. The commercially significant shift is from AI that scores leads for a human to review, to AI that autonomously executes the next action. A high-intent buyer is identified, contacted, pre-qualified, and booked for a test drive before a salesperson is involved. The F&I conversation that follows is with a different kind of customer.

Fixed operations and inventory intelligence is generating 15–20% service revenue increases in documented deployments through predictive outreach — identifying vehicles approaching failure thresholds before the customer knows there is a problem and initiating contact proactively.

What the M&A Activity Is Telling Us

Deal flow in AI dealertech accelerated materially in 2024 and 2025. Warburg Pincus made a strategic growth investment in myKaarma, an AI-enabled fixed ops platform, in January 2026. Francisco Partners acquired OEConnection, an AI aftersales tech platform, in November 2025. Dealer Tire invested in BizzyCar, a recall management and mobile service AI platform with over $50 million in total funding, in September 2025. Woven Capital led a $191 million Series D extension into UVeye, an automated vehicle inspection company with $380.5 million in total funding, in January 2025.

The pattern across transactions is consistent. Acquirers are prioritizing proprietary dealer data networks that compound over time, deep DMS integration with genuine write-back capability, and workflow ownership rather than point functionality. Platforms that own and execute the workflow — not just assist or analyze — are commanding the valuations. Point solutions that have not expanded beyond a narrow use case are increasingly becoming acquisition targets rather than long-term standalone businesses.

For administrators and F&I professionals, the M&A signal is worth reading directly: the infrastructure around your book of business is being rebuilt. The question is not whether that affects your operation. It is how quickly you engage with what is being built.

Further Reading

For a detailed look at the AI capability stack now being assembled across automotive retail — including company profiles, a breakdown of each capability category, and the full M&A transaction history — the source for much of the data in this piece is the Colonnade Advisors DealerTech M&A Landscape report, published March 2026: DealerTech M&A Landscape: AI Impact.

Dark Sky Data provides data and analytics solutions for F&I professionals, warranty administrators, and dealership finance operators.